How to design retirement benefits to build wealth, reduce taxes, & support staff without turning plan administration into a second job.

For many practice owners, offering retirement benefits may be important, but can be confusing or become administratively burdensome. Whether or not you choose to offer retirement benefits, it may be costing you thousands in missed tax-saving opportunities, hidden fees, and administrative time.

A strategically designed retirement plan is one of the most powerful wealth-building and tax-saving tools available for practice owners. It can also be a differentiator to attract and retain exceptional team members in a competitive market. Providing retirement benefits in your practice can boost staff morale, reduce their financial stress, and show you truly care about their financial future.

This guide reflects our experience helping dental practices design retirement benefits that work for them while not increasing their administrative workload.

Every practice owner should ask themselves these 3 questions:

- Do I have the right type of retirement benefits for my practice?

- Are the fees I am paying reasonable and clear?

- Am I getting service that fits my needs and saves me time?

Your retirement benefits are like crown prep: the design matters, margins matter, and a poor fit becomes expensive and frustrating.

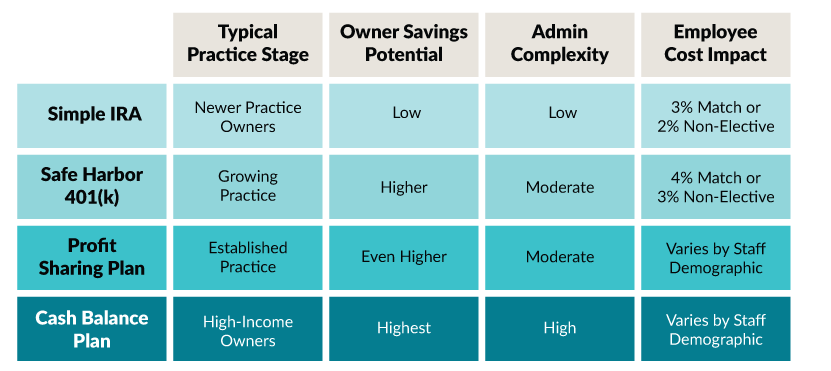

Do I have the right type of retirement benefits?

Different plan types may fit different stages of practice growth. Many dental practices follow a natural progression as their profitability increases:

They start with a SIMPLE IRA and eventually switch to a 401(k) for greater savings potential. If desired, they can add a Profit-Sharing element or even a Cash Balance plan on top of their existing 401(k) plan.

SIMPLE IRA

A strong starter option for dentists who recently purchased a practice and want to offer benefits with minimal administration and cost.

Safe Harbor 401(k)

As cash flow stabilizes and profitability improves, many owners transition to a 401(k) to unlock higher savings potential. IRS startup tax credits now offset setup costs for several years, making this a viable starter option as well.

Add Profit-Sharing Plan

When additional discretionary income is available, tax-deductible Profit-Sharing contributions can be layered onto the 401(k). The contributions only come from the owner and are optional each year, and the amounts contributed to owners versus their employees can vary based on staff demographics. A common goal is to maximize owner contributions while keeping employee contributions reasonable. These contributions are subject to a vesting schedule, encouraging employee retention.

Add a Cash Balance Plan

If the owner wants to shelter more income, especially in higher tax brackets, a Cash Balance plan may be appropriate. These plans are more complex and work best with an experienced administrator and advisor team. When implemented properly, they can significantly increase tax-deductible contributions.

– PLANNING TIP –

If your spouse works in the practice (or supports it in a documentable way), consider asking your CPA about adding them to payroll so they can participate in retirement benefits too. This can significantly increase household tax-advantaged savings!

Key Questions to Consider

Are your current benefits aligned with:

- Your profitability

- Your tax bracket

- Your retirement timeline

- Your staff demographics

Am I getting service that fits my needs and saves me time?

Offering retirement benefits adds responsibilities to your plate that requires time and oversight. Hiring the right team of professionals to help with those responsibilities can keep retirement benefits at your practice running smoothly.

One way to think about your support team for your retirement benefits is as a basketball team: each player has a unique, specific role, and weak performance in one area affects the whole team. After all, legendary basketball coach Pat Riley once said, “The key to teamwork is to learn

a role, accept a role, and strive to become excellent playing it.”

Plan Administrator

- Maintains IRS compliance

- Helps design and optimize your retirement plan

- Files annual tax form 5500

- Generates required notices to be delivered to employees

Recordkeeper

- The online “hub” of your retirement plan

- Tracks transactions and contributions

- Integrates with your payroll system for automated contributions

- Processes account updates online (contribution rates, beneficiary updates, withdrawals, etc.)

Financial Advisor

- Selects and monitors investment options

- Evaluates retirement benefits design relative to your personal financial goals

- Provides personal, comprehensive financial planning for doctors

- Provides investment and financial advice for staff members

- Coordinates annual staff education & enrollment meetings

Bookkeeper

- Updates payroll when staff members change how much they contribute

- Processes deposits into retirement plan accounts

Custodian

- Holds the assets and provides investment brokerage services

Retirement benefits function best when each responsibility is clearly covered. Some practices attempt to operate without support in certain roles, which can lead to inefficient administration and frustration for owners and employees alike.

For example, if an office does not have a financial advisor to conduct annual education and enrollment meetings or to provide investment and financial guidance to staff, employees may be less likely to understand or utilize their retirement benefits. This can lead to lower appreciation of the benefits offered and frustration from unanswered questions. Partnering with a financial advisor helps increase employee engagement, ensuring the retirement plan is viewed as a valuable benefit and an effective retention tool rather than an afterthought.

Key Questions to Consider

Who’s on your team? What responsibilities do you have?

Are the fees I am paying reasonable and clear?

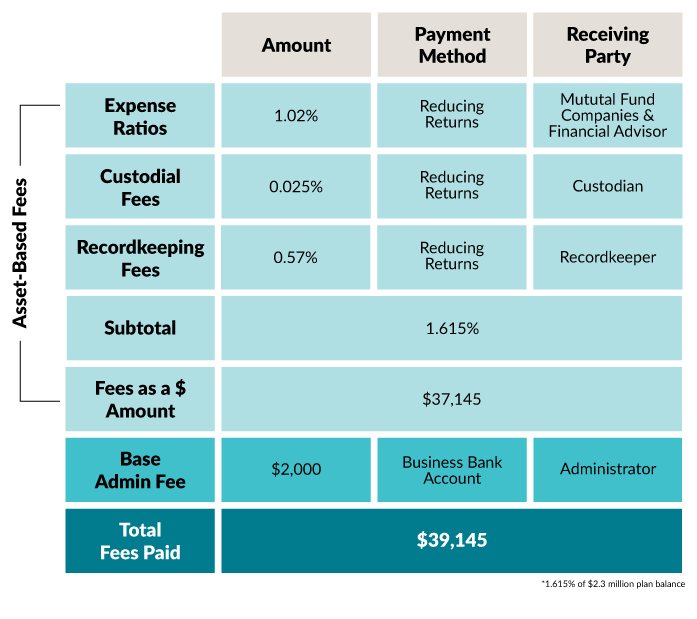

While some fees are very clear and visible, some fees can be harder to spot. For example, in a recent fee analysis, a two-doctor practice believed they paid $2,000 in annual retirement benefit fees, but were actually paying almost $40,000 (Keep reading to see why!).

Offering retirement benefits can involve multiple service providers, and fees can be charged in multiple ways, sometimes making fees unclear. A proper analysis of your fees answers two questions:

Who is getting paid?

- Plan administrator

- Custodian

- Recordkeeper

- Financial Advisor

- Investment product expenses

How are they getting paid?

- Billed directly to your business bank account (Easily Noticeable)

- Deducted directly from retirement accounts (visible as transactions on statements).

- Reducing your investment returns (common for mutual fund/ETF expense ratios; less noticeable)

Reviewing fee disclosure documents, account statements, and provider invoices together helps clarify total costs. When we do this analysis, we often break out the fees into:

- Asset-based fees (percentage of assets)

- Dollar-based fees (flat or per participant fee).

Because payment structures vary widely, total cost is not always obvious. Below is a chart showing an example from the two-doctor practice previously referenced.

Notice how all the asset-based fees in the chart below were reducing investment returns. Knowing exactly who you are paying and what you are paying them is essential!

Key Questions to Consider

How much are you actually paying in total fees (including the ones who are less visible)?

Who are you paying fees to? How are your fees being paid?

Conclusion

The correct answers to each of the three overarching questions in this guide are unique to each practice and doctor.

Knowing the answers for yourself will keep you on track for your financial goals and provide you with peace of mind about your financial future.

At Financial Freedom for Dentists, we help practice owners answer these questions. As independent financial advisors and fiduciaries, we guide dentists toward solutions tailored to their practice and financial situation.

Want to compare a SIMPLE IRA, 401(k), profit sharing or cash balance plan? Freedom For Dentists will review your current plan design, fees, and service level at no cost to you. Reach out today for your Complimentary Retirement Benefits Analysis.

Call 425.888.1911. Email Info@Freedom4Dentists.com or schedule your analysis directly.

![]()

Written by Financial Freedom for Dentists

Published in Catalyst – Q2 2026.

Advisory services are offered through Financial Freedom for Dentists LLC, an SEC Investment Advisor. All content is for information purposes only. It is not intended to provide any tax or legal advice or provide the basis for any financial decisions. Nor is it intended to be a projection of current or future performance or indication of future results. Investing always involves risk and possible loss of capital.

Category: Practice Consulting

Back to Articles